Hyperliquid’s Ecosystem Fractures

“Wishing every day for a @YBSBarker tech cofounder to appear.

When fortune favors, all things work together; when fortune fades, heroes are powerless.

Binance has launched Aster to attack Hyperliquid’s OI and trading volume; $JELLYJELLY and $POPCAT have launched consecutive attacks on HLP, but these are just minor irritations;

Amid the booming HIP-3 growth mode, the rumored BLP (lending protocol), and the news of $USDH proactively staking 1 million $HYPE to become aligned quote assets, Hyperliquid is starting to show its own cracks—the HyperEVM ecosystem and $HYPE are not yet aligned.

Alignment isn’t complicated; under normal circumstances, the HyperEVM ecosystem consumes $HYPE, and $HYPE would also support the HyperEVM ecosystem’s development.

Currently, things are not normal. The Hyperliquid Foundation’s main focus is still on HyperCore’s spot, derivatives, and utilizing HIP-3 markets for $HYPE ; the development of the HyperEVM ecosystem remains a second-class concern.

Earlier, a third-party HIP-5 proposal suggested allocating some of $HYPE ’s buyback fund to support ecosystem project tokens, but this was met with broad community rejection and skepticism. This points to a harsh reality: $HYPE ’s current price is entirely supported by HyperCore market buybacks, with no extra capacity to support the HyperEVM ecosystem.

Lessons from Elsewhere: Ethereum’s Scaling Successes and Failures

“L2 shifting to Rollups hasn’t satisfied ETH, and third-party sequencers are almost absurd.

The development of a chain involves three parties: the main token (BTC/ETH/HYPE), the foundation (DAO, figurehead, company), and the ecosystem project teams.

Among these, the interaction model between the main token and the ecosystem projects determines the chain’s future:

- Main token ⇔ ecosystem: two-way interaction is healthiest; the ecosystem needs the main token, and the main token empowers ecosystem projects. SOL does this best right now;

- Main token → ecosystem: the main token unilaterally empowers the ecosystem; after TGE, the main token disperses—typical examples are Monad or Story;

- Ecosystem → main token: the main token drains value from ecosystem projects, with the ecosystem in a competitive-cooperative state with the main token.

The evolving relationship between Ethereum and its DeFi projects and L2s is the most direct example. It also reflects HyperEVM’s current reality and possible future breakthroughs.

According to 1kx research, the top 20 DeFi protocols account for about 70% of on-chain revenue, but their valuations are far lower than the underlying chain. The “fat protocol” theory still lingers, and people trust Uniswap and stablecoins on Ethereum more than stand-alone chains like Hyperliquid and USDe.

Not to mention that Vitalik has long “disliked” DeFi yet can’t do without it, ultimately awkwardly coming up with low-risk DeFi theories. Many DeFi protocols have tried to build their own portals, from dYdX V4 to MakerDAO’s 2023 EndGame plan, with technical approaches spanning Cosmos, Solana, and other AltVM systems.

Then came Vitalik’s public sell-off of $MKR . Beyond the main token-ecosystem interaction, people have long underestimated the “official” legitimacy of public chains, especially that conferred by spiritual leaders.

Vitalik, representing the EF (Ethereum Foundation), has long let DeFi develop freely, focusing instead on philosophical ideas. While the ecosystem and the foundation struggle, Solana DeFi’s rise is no coincidence. Ultimately, Hyperliquid is striking out with an exchange+public chain model, taking chain competition to a new level.

Solana’s challenge to Ethereum has brought criticism to Vitalik and the EF, but outside of DeFi, the gains and losses of L2 scaling are even more thought-provoking. The L2/Rollup path hasn’t failed technically, but siphoning off L1 revenue has pushed ETH into a downturn.

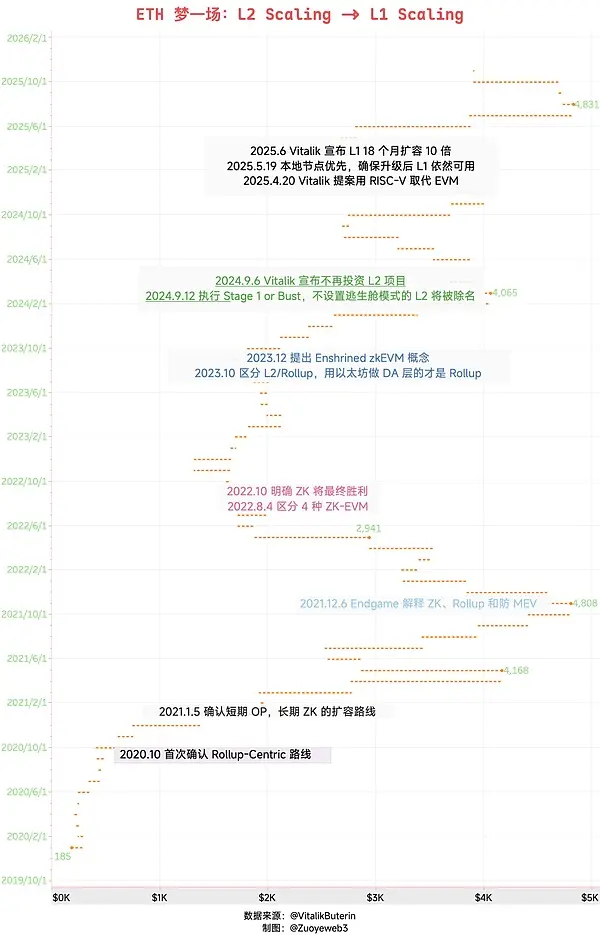

Image caption: ETH’s Dream: L2 Scaling -> L1 Scaling

Image source: @zuoyeweb3

When Ethereum L1 faced scaling pressure after the DeFi boom, Vitalik decreed a Rollup-centric approach and went all in on ZK’s long-term value, driving industry, capital, and talent into ZK Rollup FOMO. From 2020 to 2024, this created countless fortunes and tragedies.

But there’s a point: DeFi is a real product for end-users, and the proliferation of L2s essentially consumes Ethereum L1’s infrastructure resources, dividing ETH’s value capture. As 2024 marks the end of the L2/Rollup era, 2025 is set for a return to L1 scaling.

Four years away, and still back to L1 as the main path.

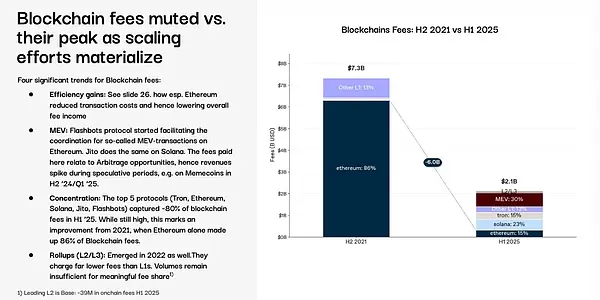

Image caption: Faster, cheaper—but at the cost of own revenue

Image source: @1kxnetwork

On the technical side, ZK and L2/Rollups do relieve L1’s burden, speeding up and lowering fees to benefit all participants, including regular users. But beyond the public chain<>DeFi (application) competitive-cooperative relationship, economically, a complex triangle of public chain<>L2<>application is created—ultimately a lose-lose-lose.

Ethereum loses revenue to L2s, L2s fragment wealth effects, and applications scatter focus trying to expand across L2s.

In the end, Hyperliquid ends the disputes with a unified stance: “the public chain is the application, and the application is trading.” Even Vitalik has lowered his head, reorganizing the EF (Ethereum Foundation) to re-embrace user experience.

During the shift from L2 to L1, technical choices at certain points—like Scroll’s appreciation of four ZK EVMs, Espresso’s bet on decentralized L2 sequencers—were ultimately disproven, while Brevis has gained attention recently because Vitalik has re-emphasized ZK’s importance for privacy, which is no longer related to Rollups.

A project’s fate depends not only on its own efforts but also on the course of history.

With dazzling victories, Hyperliquid is now encountering the same dilemma as Ethereum: how should it handle the relationship between its main token and its ecosystem?

A Modest Proposal: HyperEVM’s Alignment Choices

“BSC is a Binance subsidiary; what exactly is HyperEVM to Hyperliquid? The team hasn’t figured it out.

In the article “Creating Waves with HyperEVM,” we discussed Hyperliquid’s unique development path: first building the controllable HyperCore, then the open HyperEVM, and linking the two with $HYPE .

Looking at recent developments, the Hyperliquid Foundation insists on centering empowerment on $HYPE , maintaining a tokenomics model with HyperCore as the main body and multiple HyperEVM ecosystems developing together.

This raises the core concern: How should HyperEVM take its own unique development path?

The BSC ecosystem is a subsidiary of Binance’s main site and $BNB , with PancakeSwap, ListaDAO, and others swaying with Binance’s will, so there’s no real competition between BNB and BNB Chain.

Even Ethereum can’t maintain a lasting balance between ETH and a flourishing ecosystem. In comparison, Hyperliquid’s current problems can be summarized as follows:

- No synergy established between HyperEVM and HyperCore, making HyperEVM’s position awkward

- $HYPE is the sole concern of the Hyperliquid Foundation, leaving HyperEVM ecosystem builders somewhat at a loss

Before answering, let’s look at HyperEVM’s current state. It’s clear that HyperEVM ecosystem projects aren’t keeping up with the Hyperliquid team’s vision.

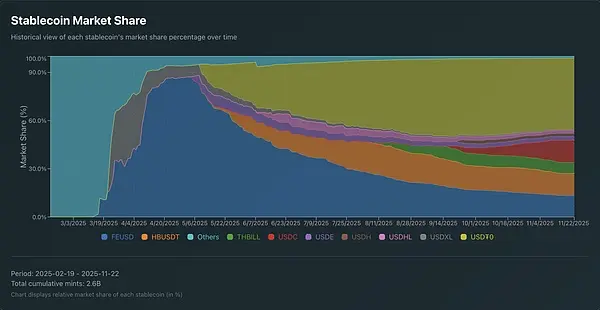

Image caption: HyperEVM stablecoin market share

Image source: @AIC_Hugo

The USDH team election triggered FOMO among stablecoin teams, but current HyperEVM stablecoin projects have no significant advantage. BLP may also have potential conflicts of interest with existing lending protocols, and the HIP-5 proposal saw almost no support for HYPE tokens empowering ecosystem projects.

$ATOM is a bitter pill for the Cosmos team; $HYPE is an illusion for ecosystem builders—no matter how much they do, it’s just consumables.

A classic question confronts HyperEVM ecosystem builders: What if Hyperliquid builds it themselves?

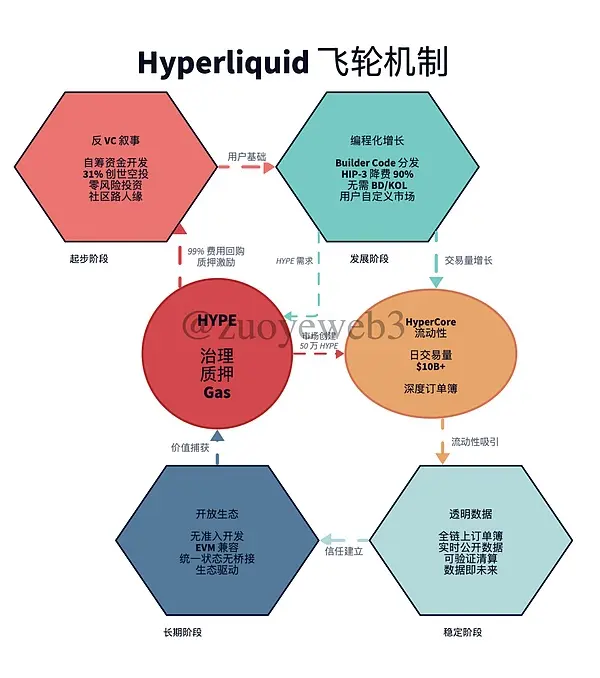

Image caption: Hyperliquid flywheel

Image source: @zuoyeweb3

Looking at Hyperliquid’s usual approach, the team excels at making moves during industry crises, thereby building its own anti-fragility. During bear markets, not only is user acquisition cheaper, but they also market their own robustness in reverse, gradually building a strong community consensus.

- In the early stage, an anti-VC narrative emphasizing self-funding and entrepreneurship, though still partnering with MMs and selling tokens to VCs, won strong grassroots support to attract early users;

- During growth, marketing strategies avoided hiring BDs to lure KOLs with commissions, instead making everything programmable (Builder Code/HIP-3 Growth Mode), giving users full customization;

- At maturity, maximizing data transparency—Hyperliquid’s latest blockchain contribution, beyond decentralization (few, centralized nodes, company-driven governance), is letting transparent data represent the chain’s future;

- In the long term, HyperEVM openness: don’t build chain ecosystems based on personal trust, but drive ecosystem growth with fully permissionless access.

The problem lies in the long-term vision: The Hyperliquid Foundation and $HYPE ’s interests are fully aligned, but to some extent, HyperEVM wants to prioritize its own token and ecosystem. This is understandable—on-chain ecosystems are always a game of trading liquidity for growth.

Governance mechanisms can’t keep up with the demands of technical innovation. From Satoshi walking away, to Vitalik’s praise and then rejection of DAOs, to the foundation model, public chain governance is still an ongoing experiment.

In a sense, Vault Curators also embody the contradiction between technology and mechanism, constantly absorbing real-world governance into the chain: lawyers + executives + BD, and on-chain “big company disease” can be even more abstract than Silicon Valley or Zhongguancun.

At least Hyperliquid’s team is closer to blockchain’s technical nature with “everything programmable”—on-chain is naturally trustless, so don’t waste effort building trust models. But even this requires extra push on HyperCore, for example in HLP management; in a crisis, manual intervention may still be needed.

At present, HyperEVM hasn’t truly achieved “permissionless” governance or liquidity. This isn’t because Hyperliquid is technically limiting it, but because legitimacy hasn’t been fully handed over to the community.

We will witness, in the coming bear market, whether HyperEVM and $HYPE can co-evolve—or whether Hyperliquid will regress into just another Perp DEX.

Conclusion

“Our ETH, Hyperliquid’s problem.

Ethereum’s health bar is thick; after PoW to PoS, L2 Scaling to L1 Scaling, and the impact of Solana in DeFi and Hyperliquid in DEX, it still holds an unbreakable market position.

$ETH has already survived bull and bear cycles, but $HYPE hasn’t yet faced a real bear market test. Sentiment is a precious consensus—the time for $HYPE and HyperEVM to align is running out.