Ethereum chooses an anti-mainstream VC route, with Vitalik Buterin emphasizing decentralization and sovereignty, while warning about long-term structural risks of USD stablecoins, oracles, and staking yields.

Going Against the Trend: The Clash Between Ethereum and Mainstream Venture Capital Strategies

In the current cryptocurrency market, which pursues quick profits and centralized efficiency, Ethereum seems to be walking a unique and solitary path.

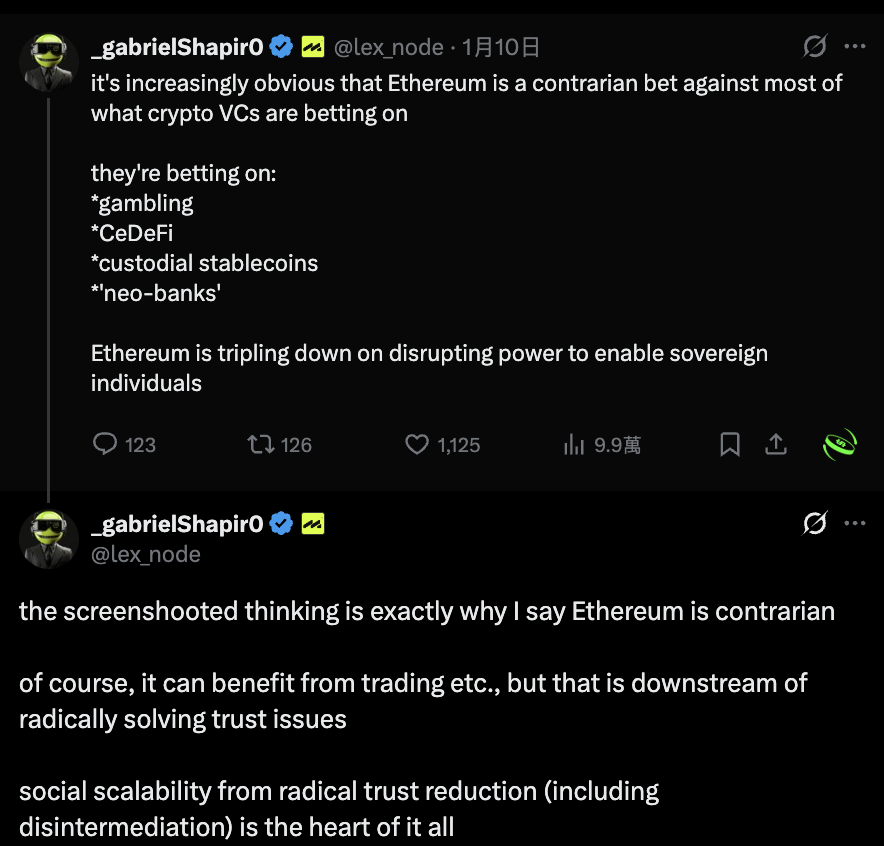

Renowned crypto legal expert and MetaLeX founder Gabriel Shapiro recently posted that Ethereum is becoming a “counter-trend bet,” with core principles that differ sharply from most venture capital (VC) strategies. Currently, mainstream VC funds are rushing into gambling applications, CeDeFi, custodial stablecoins, and various new crypto banks (Neo-banks), projects often sacrificing decentralization for short-term value capture.

Image source: X/@lex_node MetaLeX founder Gabriel Shapiro recently stated that Ethereum is becoming a “counter-trend bet.”

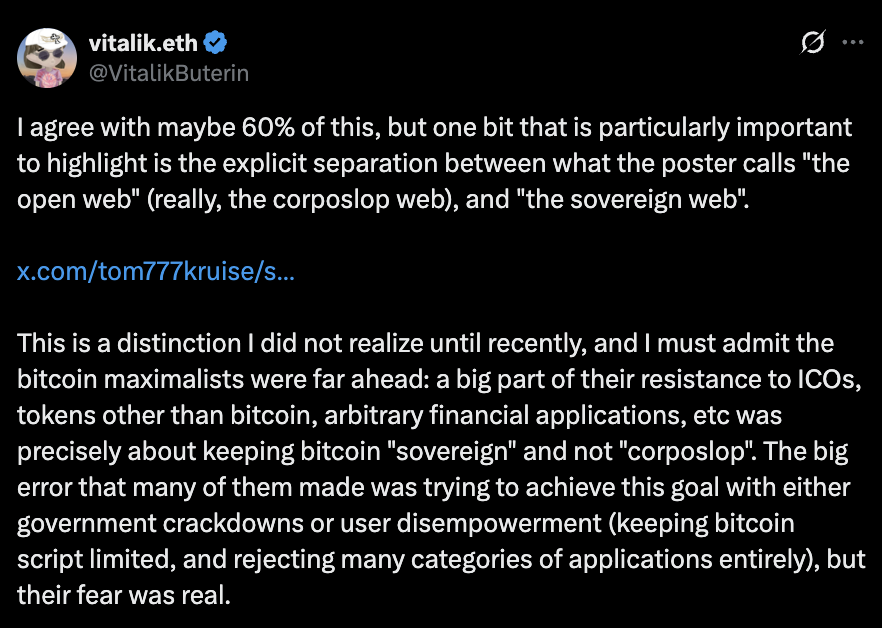

Ethereum founder Vitalik Buterin (V God) strongly agrees with this view, further pointing out that Ethereum is “doubling down” on decentralization, aiming to empower individual sovereignty. Vitalik has even expressed a certain respect on social media for the “Bitcoin Maxis,” praising their foresight in resisting corporate encroachment (Corposlop).

The so-called “Corposlop” refers to toxic products that appear user-centric but are actually designed to strip users of power.

Image source: X/@VitalikButerin Vitalik even expressed a certain respect on social media for the “Bitcoin Maxis,” praising their foresight in resisting corporate encroachment (Corposlop).

Although Vitalik criticizes some Bitcoin supporters for attempting to achieve their goals through government suppression or script restrictions—viewing this as a mistake—he admits that their fears of maintaining “sovereignty” rather than “corporatization” are genuine and reasonable. In this long-term fight to defend decentralization, Ethereum is seen as one of the last lines of defense, even though the path to true decentralization is arduous and slow.

USD Dependency Syndrome: The Long-term Lack of Risk Resistance in Stablecoins

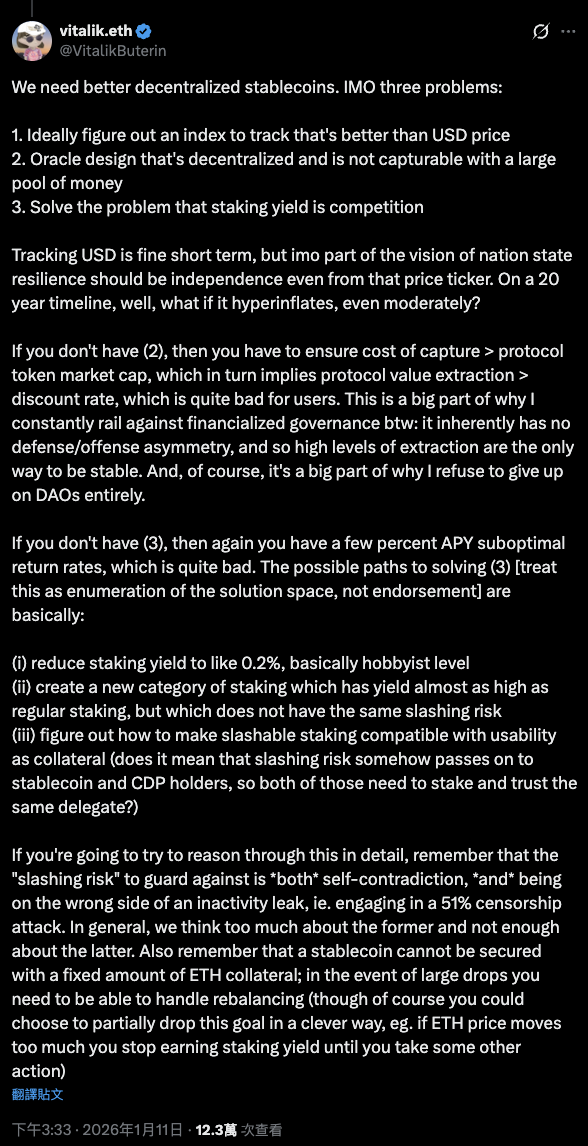

Regarding the current development of decentralized stablecoins, Vitalik raises the first profound question: Are we overly dependent on the US dollar as a benchmark?

Image source: X/@VitalikButerin Vitalik points out the current state of USD stablecoin development and raises three major questions.

He admits that tracking the USD exchange rate is feasible and convenient in the short term, but if we aim for long-term system resilience, stablecoins must learn to be independent of a single fiat currency. If the goal of decentralized finance is to build a system capable of withstanding political or economic shocks, then tying its value indefinitely to a single country’s currency clearly involves significant dependency risks.

Vitalik warns that, with the potential devaluation (Debasement) of the dollar or mild hyperinflation over the coming decades, such pegging will become a systemic vulnerability. For stablecoin designers, this is not merely a technical issue but also a matter of how to define “stability.”

He suggests that future stablecoins should explore tracking broader price indices or purchasing power standards rather than solely pegging to the USD. He believes this shift is key to protecting users from single-currency crises and is one of the reasons he has long opposed excessive “financialized governance.”

In Vitalik’s view, without governance structures that are asymmetric in defense and offense, stability can only be maintained through high-value extraction, which aligns with his core belief in not abandoning the principles of decentralized autonomous organizations (DAOs).

Oracle and Governance Traps: How to Prevent Large Capital “Soft Capture”

The second major challenge facing decentralized stablecoins is the design of oracles. Oracles are responsible for inputting real-world data (such as asset prices) into the blockchain and are central to smart contract operation.

However, Vitalik sharply points out that if an oracle mechanism can be manipulated or “captured” by large capital, the security of the protocol becomes dangerously weak. When oracle defenses are fragile, protocols often resort to extreme measures to increase attack costs, such as raising fees, issuing large token incentives, or establishing highly centralized governance structures.

This value extraction under the guise of security actually erodes user interests. Vitalik criticizes that many token-based decision-making financial governance models lack inherent defensive advantages and tend to evolve into rent-seeking structures, merely charging users high costs to sustain basic operations.

He emphasizes that the industry urgently needs a truly decentralized oracle system with “resistance to capture.” Only when attack costs exceed the protocol’s total market value and do not rely on excessive exploitation of users can decentralized stablecoins have a sustainable long-term foundation. Such technological breakthroughs are more important than any short-term financial incentives.

Staking Yield Competition: The Triangle of Security, Returns, and Liquidity

Finally, Vitalik highlights an invisible pressure faced by stablecoins in the Ethereum ecosystem: the direct competition of staking yields (Staking Yield).

After Ethereum shifted to proof-of-stake (PoS), staking ETH ($ETH) can generate stable returns, creating a significant challenge for decentralized stablecoins in attracting collateral. If users lock their ETH into stablecoin protocols but cannot earn comparable yields to direct staking, it becomes an economically suboptimal choice, making it difficult to attract large-scale long-term capital.

To address this conflict, Vitalik proposes several exploration directions: including drastically reducing staking rewards to around 0.2%, creating a new type of staking that offers high returns with lower slashing risks, or researching how assets with slashing risks can serve as qualified collateral for stablecoins.

He emphasizes that industry understanding of “slashing risk” is overly simplistic, often focusing only on malicious node behavior, while neglecting more severe risks such as inactivity leaks caused by prolonged offline periods or penalties from 51% attack validations. Stablecoin design must consider asset reorganization and balancing mechanisms under these extreme scenarios, rather than relying solely on fixed over-collateralization ratios.

For Vitalik, until these core issues are addressed, any so-called “perfect” solution is likely just a “band-aid” rather than a fundamental fix in his eyes.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.