#EUPlansCentralBankStablecoin

The European Union's central bank-backed stablecoin project has become an increasingly discussed and followed topic in recent years.

🤔 What is a Digital Euro?

A digital euro will be a digital version of the physical euro banknotes and coins we know. It will be issued by the European Central Bank (ECB), meaning it will be a currency under state guarantee.

It will be digital, like the money in your normal bank account, but it will come directly from the ECB instead of banks.

It will not replace cash, but will complement it.

It is designed to be used both online and offline (for example, payments can be made by bringing phones close together).

Everyone (citizens, tradesmen, companies) will be able to use it, and basic uses will be free.

In short: You will be able to do the same thing with your phone without taking out the 20 euros in your pocket.

Why is there a need for such a thing?

Europe faces the following problems:

A large portion of payments go through American companies such as Visa and Mastercard.

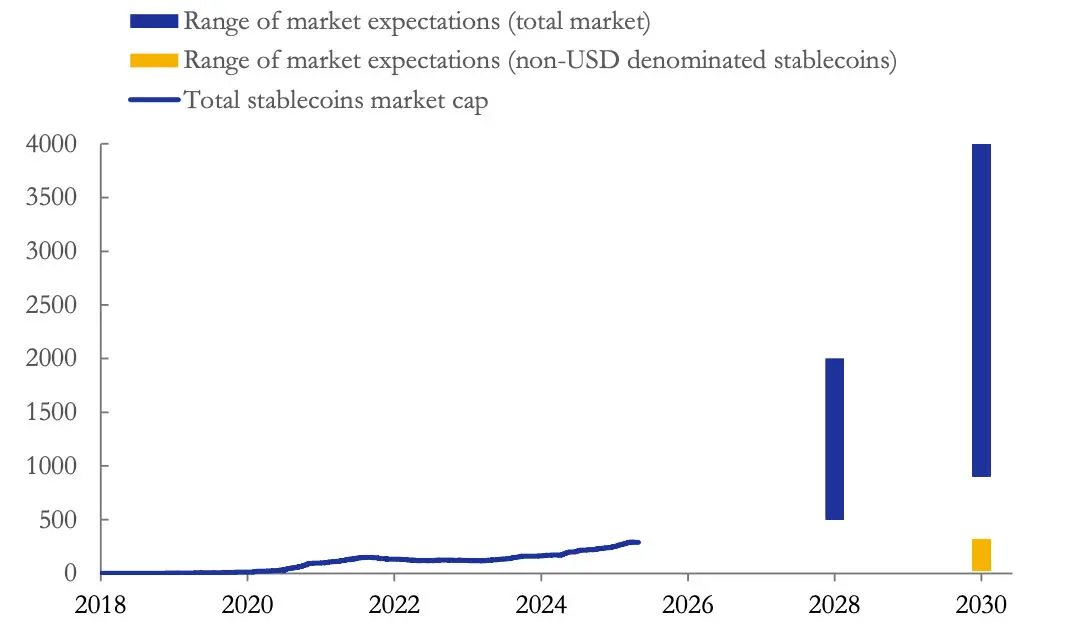

Stablecoins issued by private companies (especially those pegged to the dollar) are growing rapidly and could take control of the Eurozone.

Cash usage is decreasing, and in a completely digital world, the central bank's currency (euro) could disappear.

Europe wants to maintain its independence in the payment system.

ECB President Christine Lagarde and other officials say, "Europe needs to keep its own currency strong in the digital world as well." Otherwise, we will become more dependent on foreign companies and the dominance of the dollar.

What is the Current Situation?

The project has progressed considerably, but there is no digital euro in circulation yet. Here is the latest situation:

2023-2025: Research and preparation phase completed.

October 2025: The ECB moved the project to the next stage. Technical infrastructure is being developed, and tests are being conducted.

December 2025: The EU Council (member states) issued a joint opinion on the digital euro law.

February 2026: The European Parliament also largely supported it, approving its online and offline use.

Currently: Final negotiations are underway between the European Parliament and the Council regarding the legal framework (Regulation). Some MEPs (particularly under pressure from Germany) want changes to the details, so there are minor delays, but the overall atmosphere is positive.

Target timeline:

If the law is passed in 2026,

Pilot implementation (tests limited to individuals) will begin from mid-2027.

They plan to make the first real digital euro available in 2029.

Estimated cost: Approximately €1.3 billion for development, then around €320 million in annual operating costs (to be covered by the ECB and national central banks).

Who will participate, how will it be used?

Banks and payment companies will distribute the digital euro (meaning you will access it from your bank app or wallet).

The ECB will set holding limits to avoid distorting bank competition (e.g., one person cannot hold too many digital euros).

Privacy is important: It can be anonymous like regular cash, but there will be rules that allow for tracking in large amounts. The ECB is also conducting special studies on accessibility for the elderly and people with disabilities (for example, in cooperation with a Spanish foundation).

In short, what should we expect?

If the digital euro arrives:

Faster, cheaper and more secure intra-European payments will be made.

Thanks to the digital version of cash, not everyone will be excluded from the digital economy.

Europe will be somewhat more independent in its payment system.

But we are only at the beginning of the road.

The European Union's central bank-backed stablecoin project has become an increasingly discussed and followed topic in recent years.

🤔 What is a Digital Euro?

A digital euro will be a digital version of the physical euro banknotes and coins we know. It will be issued by the European Central Bank (ECB), meaning it will be a currency under state guarantee.

It will be digital, like the money in your normal bank account, but it will come directly from the ECB instead of banks.

It will not replace cash, but will complement it.

It is designed to be used both online and offline (for example, payments can be made by bringing phones close together).

Everyone (citizens, tradesmen, companies) will be able to use it, and basic uses will be free.

In short: You will be able to do the same thing with your phone without taking out the 20 euros in your pocket.

Why is there a need for such a thing?

Europe faces the following problems:

A large portion of payments go through American companies such as Visa and Mastercard.

Stablecoins issued by private companies (especially those pegged to the dollar) are growing rapidly and could take control of the Eurozone.

Cash usage is decreasing, and in a completely digital world, the central bank's currency (euro) could disappear.

Europe wants to maintain its independence in the payment system.

ECB President Christine Lagarde and other officials say, "Europe needs to keep its own currency strong in the digital world as well." Otherwise, we will become more dependent on foreign companies and the dominance of the dollar.

What is the Current Situation?

The project has progressed considerably, but there is no digital euro in circulation yet. Here is the latest situation:

2023-2025: Research and preparation phase completed.

October 2025: The ECB moved the project to the next stage. Technical infrastructure is being developed, and tests are being conducted.

December 2025: The EU Council (member states) issued a joint opinion on the digital euro law.

February 2026: The European Parliament also largely supported it, approving its online and offline use.

Currently: Final negotiations are underway between the European Parliament and the Council regarding the legal framework (Regulation). Some MEPs (particularly under pressure from Germany) want changes to the details, so there are minor delays, but the overall atmosphere is positive.

Target timeline:

If the law is passed in 2026,

Pilot implementation (tests limited to individuals) will begin from mid-2027.

They plan to make the first real digital euro available in 2029.

Estimated cost: Approximately €1.3 billion for development, then around €320 million in annual operating costs (to be covered by the ECB and national central banks).

Who will participate, how will it be used?

Banks and payment companies will distribute the digital euro (meaning you will access it from your bank app or wallet).

The ECB will set holding limits to avoid distorting bank competition (e.g., one person cannot hold too many digital euros).

Privacy is important: It can be anonymous like regular cash, but there will be rules that allow for tracking in large amounts. The ECB is also conducting special studies on accessibility for the elderly and people with disabilities (for example, in cooperation with a Spanish foundation).

In short, what should we expect?

If the digital euro arrives:

Faster, cheaper and more secure intra-European payments will be made.

Thanks to the digital version of cash, not everyone will be excluded from the digital economy.

Europe will be somewhat more independent in its payment system.

But we are only at the beginning of the road.