TL;DR

- The S&P 500 rose by 3.48%, while the Nasdaq gained 4.12%, as U.S.–Iran ceasefire talks intensified and mine-clearing operations began in the Strait of Hormuz.

- March CPI came in at 3.4% and PPI at 2.4% YoY, indicating persistent price pressures and complicating the Fed’s rate-cut path despite rising growth risks.

- WTI crude declined by over 14% on the week, as geopolitical risk premiums eased amid expectations of restored global supply flows.

- Crypto markets rebounded modestly, with BTC up 2.5% and ETH rising 3.9%, supported by positive spot ETF inflows.

- Among major assets, ZEC outperformed, driven by strong institutional interest linked to Grayscale’s shielded accumulation, while TON rallied following a major network upgrade that significantly improved speed and transaction finality.

- Hong Kong issued its first stablecoin licenses to Anchorpoint and HSBC, marking the launch of a regulated digital money framework.

- Japan reclassified crypto assets as financial instruments, signaling a regulatory shift toward deeper institutional market integration.

- Pharos raised $44M in strategic funding to develop financial-grade Layer 1 infrastructure bridging TradFi and DeFi.

Macro Overview

US Markets Rally as Geopolitical Tensions Ease and Tech Outperforms, March CPI and PPI Data Shows Persistent Inflationary Pressures

The March Consumer Price Index (CPI) rose 0.9% MoM and 3.4% YoY, the highest annual rate since April 2024, largely driven by energy and shelter costs. Similarly, the Producer Price Index (PPI) showed wholesale prices increasing more than anticipated. While core inflation remained somewhat stable, the headline figures underscore the ongoing impact of the energy shock stemming from the Strait of Hormuz crisis.

US equity markets extended their gains this week, with the S&P 500 rising 3.48% to close at 6,816.89. The Nasdaq Composite led the rally with a 4.12% surge, driven by strong performance in the technology sector, while the Dow Jones Industrial Average gained 2.67%. The market sentiment was bolstered by reports of intensified US-Iran peace talks. The S&P 500 and Nasdaq both reached new highs for the year, recovering nearly all of the losses from the previous month’s volatility.

Asian equities staged a broad recovery this week, mirroring the rally in Wall Street. The Nikkei 225 and Hang Seng Index both gained ground as the threat of sustained $120+ oil prices receded. Tech-heavy markets like Taiwan and South Korea benefited from the global rotation back into growth stocks. However, the Bank of Japan remains in a difficult position, with minutes showing continued pressure to normalize policy as inflation remains above target despite the yen’s recent stabilization. The MSCI Emerging Markets index outperformed developed markets for the first time in three weeks, reflecting a return of risk appetite as the geopolitical tail-risk diminished.

Despite higher-than-expected inflation data released late in the week, investors remained focused on the potential for a ceasefire in the Middle East, which triggered a significant relief rally.

The minutes from the March 18 FOMC meeting, released Wednesday, revealed a committee deeply divided on the appropriate timing for rate cuts. While most members agreed on the need to maintain a restrictive stance until inflation sustainably returns to 2%, several participants expressed concern about the downside risks to growth posed by the Iran conflict and global trade disruptions. The minutes showed that the “look-through” approach to energy shocks is the current consensus, but a vocal minority warned that persistent supply-side pressures could unanchor inflation expectations. Market pricing now suggests a high probability that the Fed will hold rates steady through the first half of 2026.

Looking ahead, market participants will pivot from geopolitical headlines to the resilience of the US consumer and the health of the manufacturing sector, depending on the progress of the peace talks. Key data releases, including Retail Sales and the Empire State Manufacturing Index, will be critical in determining if the high-interest-rate environment is finally beginning to weigh more heavily on domestic demand. While the de-escalation in the Middle East provides a constructive backdrop, the Fed’s “higher for longer” narrative is unlikely to shift until a more definitive cooling of core inflation is observed. (1)

DXY

The US Dollar Index (DXY) weakened significantly, dropping from 100.18 to 98.70. The primary driver was the easing of safe-haven demand as peace talks in the Middle East gained momentum. Despite hawkish CPI data, the dollar was unable to sustain its recent highs as investors shifted capital back into riskier assets and emerging market currencies. (2)

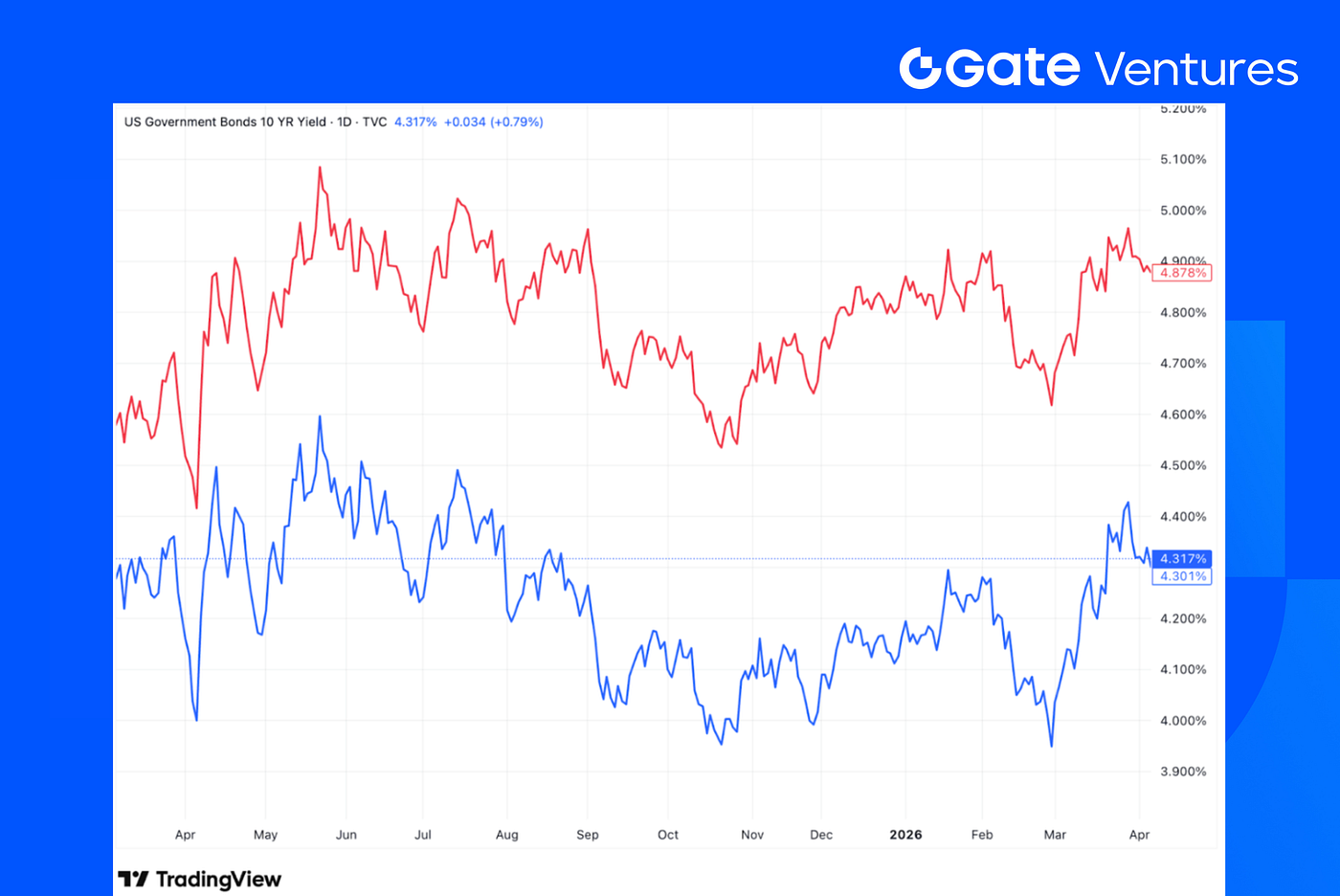

US 10-Year and 30-Year Bond Yields

Treasury yields ended the week slightly lower. The 10Y yield fell to 4.317% and the 30Y to 4.878%. Yield markets initially reacted with a spike in yields, but the focus quickly shifted back to geopolitical developments and expectations for corporate earnings as the Q1 reporting season began. (3)

Gold

Gold prices continued their ascent, closing at $4,746.90. While easing geopolitical tensions usually weigh on gold, the significant weakening of the US dollar and persistent inflation data (CPI/PPI) provided strong support. Investors continue to view gold as a critical hedge against potential stagflationary outcomes if the peace process stalls. (4)

Crypto Markets Overview

1. Main Assets

BTC Price

ETH Price

ETH/BTC Ratio

BTC rose 2.5% over the past week, while ETH outperformed with a 3.9% gain. Spot ETF flows remained constructive, with BTC ETFs recording net inflows of $786.3 million and ETH ETFs seeing net inflows of $187.1 million. (5)

The ETH/BTC ratio also moved higher, rising 1.4% to 0.0309. Despite the price rebound and positive fund flows, overall market sentiment remains fragile, with the Fear & Greed Index still deep in Extreme Fear territory at 13. (6)

2. Total Market Cap

Crypto Total Marketcap

Crypto Total Marketcap Excluding BTC and ETH

Crypto Total Marketcap Excluding Top 10 Dominance

The total crypto market cap rose 2.5% last week. However, if BTC and ETH are excluded, the rest of the market was broadly flat, up just 0.3%. This suggests that most of the gains were still driven by the two largest assets.

Meanwhile, the altcoin market, measured as total market cap excluding the top 10 tokens, rose 1.5%, pointing to some strength in smaller tokens, though the rebound was still relatively modest.

Source: Coinmarketcap and Gate Ventures, as of 13th Apr 2026

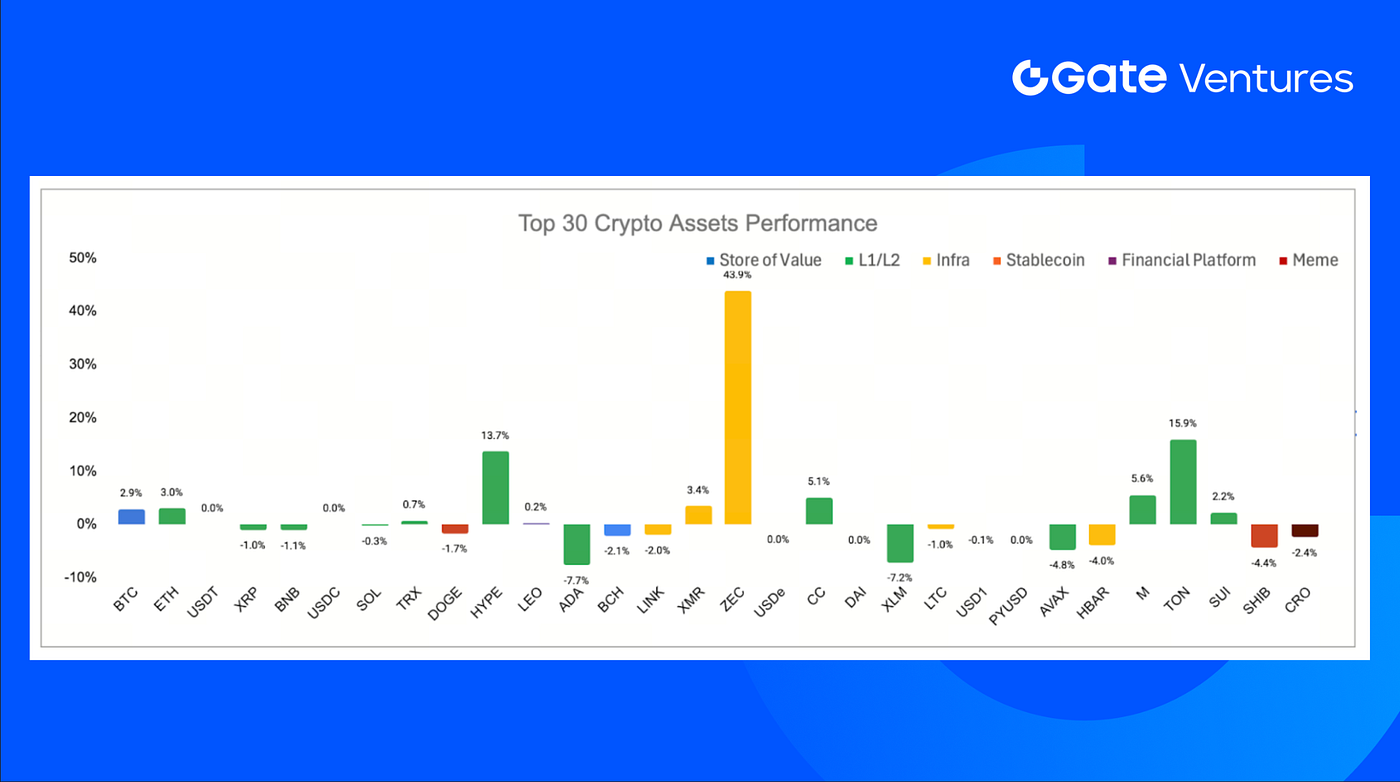

Among the top 30 assets, prices surged 1.9% on average, ZEC, TON, and HYPE led the gain.

Zcash led the market with a 43.9% gain, mainly driven by Grayscale’s accumulation of approximately $46 million in shielded ZEC, which signaled institutional conviction in Zcash’s privacy-preserving infrastructure rather than short-term speculative demand. (7)

TON followed with a 15.9% gain, supported by Telegram founder Pavel Durov highlighting a major TON network upgrade that increased block speed sixfold and reduced transaction finality to under one second. (8)

The Key Crypto Highlights

1. Bitwise moves closer to spot Hyperliquid ETF launch as competition for HYPE exposure intensifies

Bitwise Asset Management has filed a second amended registration statement with the U.S. Securities and Exchange Commission for its proposed spot Hyperliquid ETF, adding the ticker $BHYP and setting a 0.67% management fee. If approved, the fund would trade on NYSE Arca and provide direct exposure to spot HYPE, with additional yield potentially sourced from staking. The update reflects accelerating institutional positioning around Hyperliquid-linked products as asset managers race to capture demand following strong token performance over the past year. (9)

2. Hong Kong issues first stablecoin licenses to Anchorpoint and HSBC as regulated digital-money framework goes live

Hong Kong Monetary Authority has granted its first stablecoin issuer licenses to Anchorpoint Financial and The Hongkong and Shanghai Banking Corporation Limited under the city’s new fiat-referenced stablecoin regime, signaling the operational start of Hong Kong’s institutional digital-currency infrastructure. Anchorpoint is a consortium backed by Standard Chartered Bank (Hong Kong), Animoca Brands and Hong Kong Telecommunications, while HSBC’s inclusion highlights regulators’ preference for bank-anchored issuers in the initial rollout phase. (10)

3. Japan reclassifies crypto as financial instruments as regulatory shift targets institutional market integration

Japan has amended its Financial Instruments and Exchange Act to classify crypto assets as financial instruments rather than payment tools, introducing insider-trading prohibitions, stricter disclosure requirements for token issuers and tougher penalties for unregistered exchanges. The reform, led by the Financial Services Agency, reflects rising institutional participation and aligns crypto regulation with equities-style investor-protection frameworks, while supporting broader policy initiatives including a proposed 20% flat tax regime on crypto gains and plans to enable crypto ETFs by 2028 with participation expected from firms such as Nomura Holdings and SBI Holdings. (11)

Key Ventures Deals

1. Pharos raises $44M strategic funding to build financial-grade Layer 1 infrastructure for bridging TradFi and DeFi

Pharos Network is developing a financial-grade, asset-native Layer 1 blockchain designed to bridge traditional finance and DeFi across the estimated $50 trillion RWA and TradFi market, backed by strategic investors including Sumitomo Corporation’s CVC arm, SNZ Holding, Chainlink Labs and Flow Traders. Built on a deep-parallel execution architecture with native compliance features, the network targets real-time institutional settlement and high-frequency financial applications at scale, with its AtlanticOcean testnet already onboarding millions of users and forming RWA partnerships such as a solar-backed initiative with GCL Group. (12)

2. Giggles raises $1.23M to build meme-native prediction market blending social feeds with crypto trading mechanics

Giggles has raised $1,234,567 in funding led by 1kx to develop a TikTok-style social prediction platform where users invest in viral content using tokenized “aura points,” with plans to expand into crypto-based participation. Founded by teenage creator Justin Jin, the app has already attracted over 450,000 waitlist signups in invite-only beta and aims to increase engagement time by turning meme virality into a tradable signal layer. (13)

3. Enhanced Secures $1M in Strategic Pre-Seed Funding to expand structured yield infrastructure across more onchain assets

Enhanced Labs has raised $1 million in a strategic pre-seed round led by Maximum Frequency Ventures, with participation from GSR, Selini Capital and Flowdesk, to build DeFi products that package options and derivatives strategies into more accessible onchain yield solutions. The protocol is focused on improving capital efficiency and auction mechanics, expanding options-based yield beyond major crypto assets into areas such as tokenized real-world assets, and simplifying user experience around outcomes like yield generation, hedging and structured exposure. (14)

Ventures Market Metrics

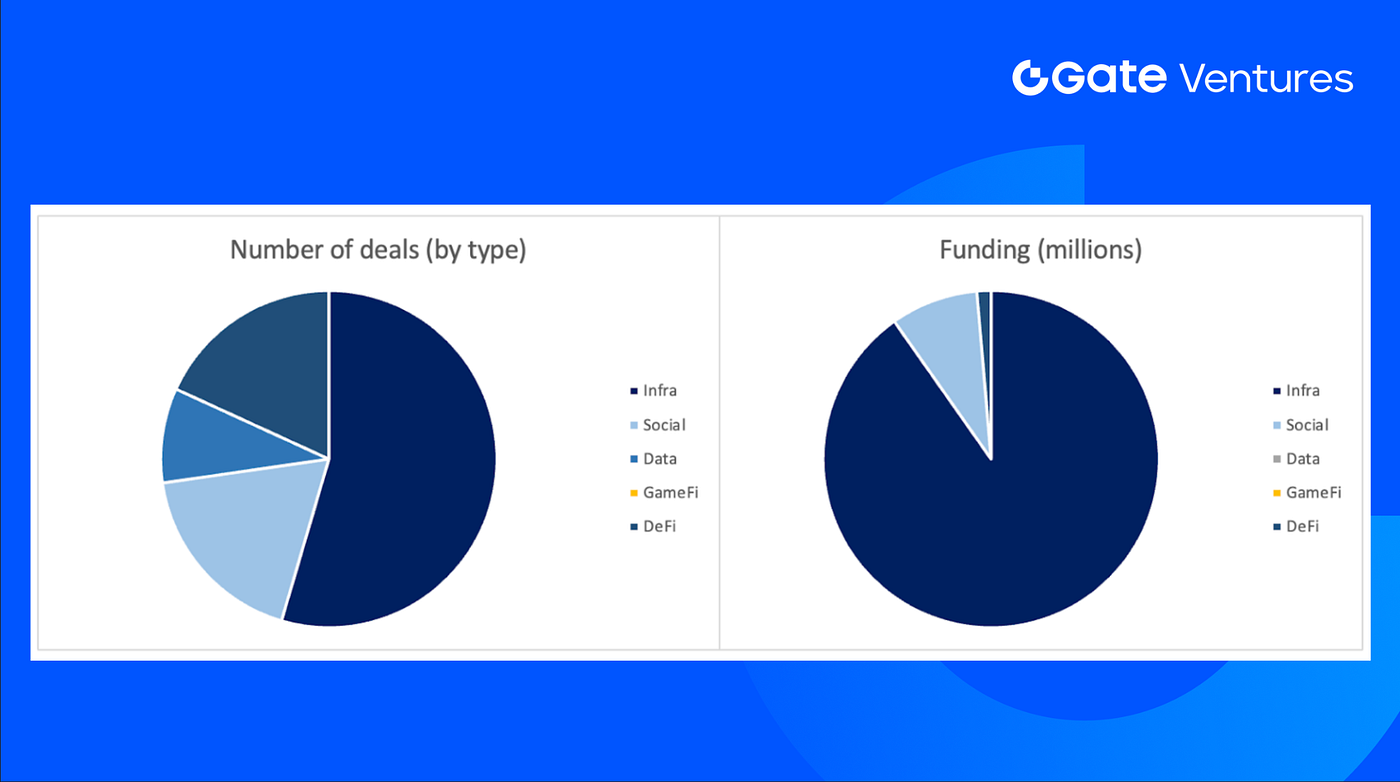

The number of deals closed in the previous week was 11, with Infra having 6 deals, Defi and Social having 2 deals respectively, and Data having 1 deal.

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 13th Apr 2026

The total amount of disclosed funding raised in the previous week was $73.7M, 5 deals in the previous week didn’t announce the raised amount. The top funding came from the Infra sector with $66.5M. Most funded deals: Pharos ($44M).

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 13th Apr 2026

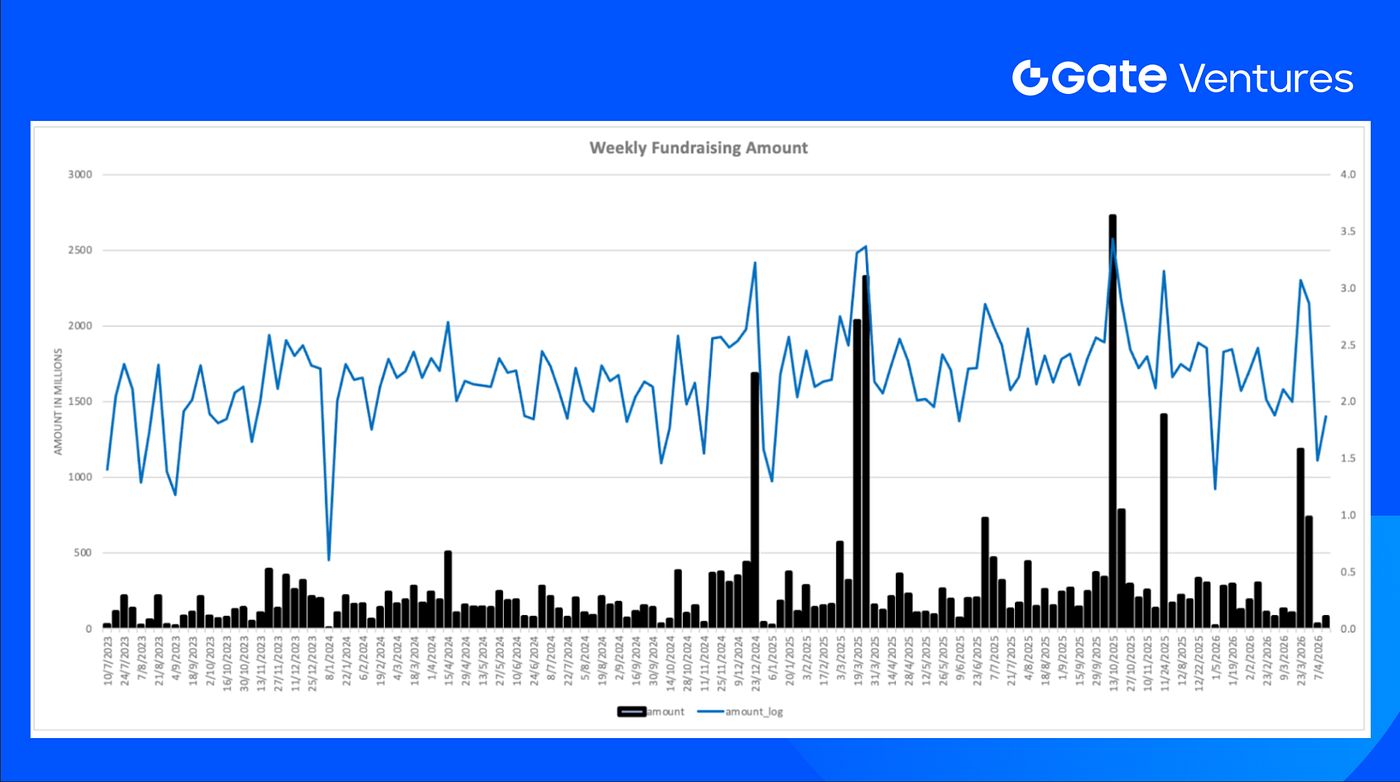

Total weekly fundraising surged to $73.7M for the second week of Apr-2026, an increase of 142% compared to the week prior.

About Gate Ventures

Gate Ventures, the venture capital arm of Gate.com, is focused on investments in decentralized infrastructure, middleware, and applications that will reshape the world in the Web 3.0 age. Working with industry leaders across the globe, Gate Ventures helps promising teams and startups that possess the ideas and capabilities needed to redefine social and financial interactions.

Website | Twitter | Medium | LinkedIn

The content herein does not constitute any offer, solicitation, or recommendation*.* You should always seek independent professional advice before making any investment decisions. Please note that Gate Ventures may restrict or prohibit the use of all or a portion of the services from restricted locations. For more information, please read its applicable user agreement.

Reference:

- Trading Economic Ahead Economic Preview, https://www.spglobal.com/market-intelligence/en/news-insights/research/2026/04/week-ahead-economic-preview-week-of-13-april-2026

- DXY Index, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3ADXY

- US 10 Year Bond Yield, TradingView, https://www.tradingview.com/chart/B9cgEklh/?symbol=TVC%3AUS10Y

- Gold Price, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3AGOLD

- BTC & ETH ETF Inflow, https://sosovalue.com/tc/assets/etf/us-btc-spot

- BTC Greed and Fear Index, https://alternative.me/crypto/fear-and-greed-index/

- Grayscale Accumulation, https://coinmarketcap.com/community/articles/69d6ab8fdac92c4e3f6aa11e/

- TON Blockchain Upgrade, https://coinmarketcap.com/community/articles/69d7d087649397091d119592/

- Bitwise moves closer to spot Hyperliquid ETF launch as competition for HYPE exposure intensifies, https://cointelegraph.com/news/bitwise-edges-closes-to-hyperliquid-etf-launch-with-second-amended-filing

- Hong Kong issues first stablecoin licenses to Anchorpoint and HSBC as regulated digital-money framework goes live, https://cointelegraph.com/news/hong-kong-first-stablecoin-licenses-issued

- Japan reclassifies crypto as financial instruments as regulatory shift targets institutional market integration, https://cointelegraph.com/news/japan-approves-bill-classify-cryptocurrencies-financial-instruments

- Pharos raises $44M strategic funding to build financial-grade Layer 1 infrastructure for bridging TradFi and DeFi, https://x.com/pharos_network/status/2041850490078818490

- Giggles raises $1.23M to build meme-native prediction market blending social feeds with crypto trading mechanics, https://techcrunch.com/2026/04/07/a-teenage-minecraft-youtuber-raised-1234567-for-a-meme-prediction-market-called-giggles-it-broke-me/

- Enhanced Secures $1M in Strategic Pre-Seed Funding to expand structured yield infrastructure across more onchain assets,

https://decrypt.co/363817/enhanced-secures-1m-in-strategic-pre-seed-funding-to-bring-structured-yield-to-more-assets-onchain