Futures

Access hundreds of perpetual contracts

TradFi

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Futures Kickoff

Get prepared for your futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to practice risk-free trading

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

TACO! Trump says "The war will end soon," U.S. stocks and bonds sharply rebound, and crude oil once plummeted 30% from the daily high

Due to concerns over a prolonged disruption of the global energy supply chain, crude oil prices surged at one point, triggering a sharp decline in global risk assets. However, as G7 finance ministers indicated possible measures to stabilize oil prices and Trump hinted that the war is “basically over” and ahead of schedule, market panic eased. Short covering and bargain hunting jointly drove risk assets to rally strongly in the late session, while crude oil prices fell significantly from the daily high.

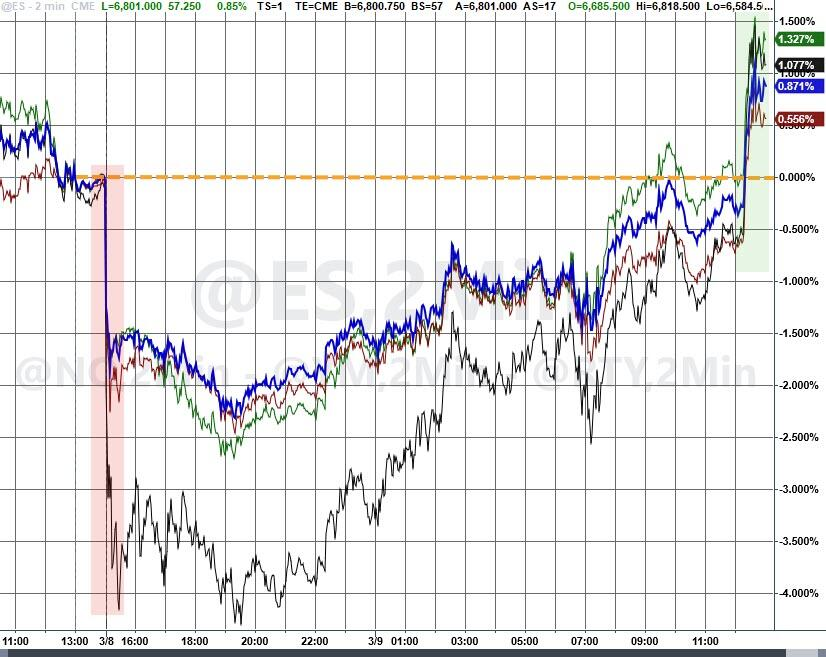

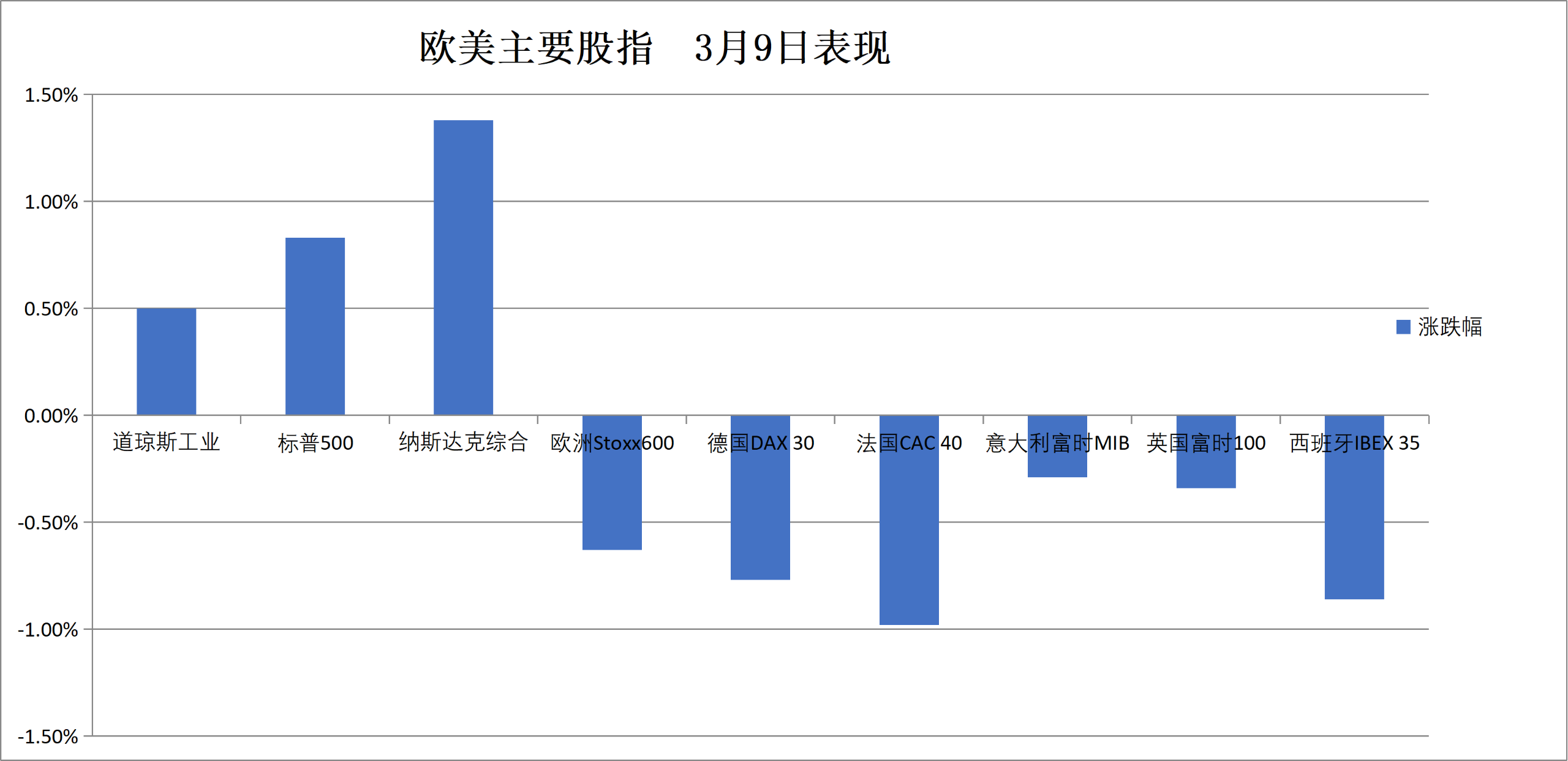

On Monday, the three major US stock indexes all closed higher, with the S&P 500 turning positive after dropping 1.5% intraday—the first time since April last year—and ending up 0.8%. The small-cap Russell 2000 index briefly fell 2.4% intraday but recovered to close up 1.12%.

( US stock benchmark indices intraday movement)

US stock benchmark indices intraday movement)

Wall Street Journal reported that only one bulk carrier related to Iran left the Persian Gulf in the past 24 hours. With shipping through the Strait of Hormuz halted, WTI crude oil prices surged nearly 30%, approaching $120. Fears of runaway inflation and recession caused US stocks to open lower.

However, the selling wave reversed during the US midday session. After an emergency video conference, G7 issued a joint statement saying they are “ready at any time” to take necessary measures to support global energy supply and stabilize prices.

Subsequently, according to CCTV News, US President Trump said in a phone interview:

Trump also said that the progress is “much faster” than his initial estimate of 4 to 5 weeks. Oil prices then accelerated their decline, with US crude dropping over 31% from the daily high and down 7% from last Friday’s close, while Brent crude fell 4.67%.

( Oil prices plummet after G7 hints at strategic reserves release and Trump’s “war over” statement)

Oil prices plummet after G7 hints at strategic reserves release and Trump’s “war over” statement)

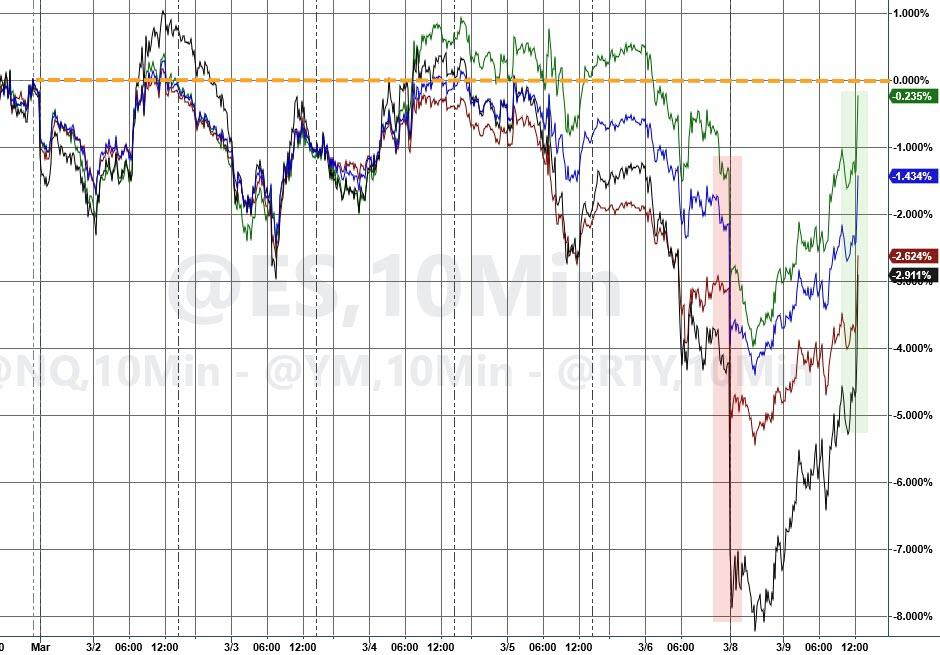

The retreat in oil prices immediately eased inflation fears weighing on risk assets. Major US stock indexes rallied strongly in the last hour, with the Nasdaq leading and essentially recovering all losses since the Iran conflict began.

( US stock benchmark indices since last Monday)

US stock benchmark indices since last Monday)

Interactive Brokers’ Steve Sosnick said:

Behind this extreme volatility is not only retail investors’ reliance on ‘buying the dip’ but also amplified by the structure of the options market.

Analysts believe that currently, US stocks are in a typical “negative gamma” state, where market makers are forced to sell during declines and quickly buy back to hedge during rebounds. This mechanical trading greatly magnifies intraday market swings.

Carol Schleif of BMO Private Wealth said:

JPMorgan’s Andrew Tyler noted that due to the war, the S&P 500 could fall as much as 10% from its peak, catching traders unprepared, and he has shifted to a “tactical bearish” stance.

Yardeni Research founder raised the probability of a stock market crash this year from 20% to 35%. He also significantly lowered the chance of a major rally from 20% to 5%. The so-called “surge” refers to a rally driven mainly by investor enthusiasm rather than fundamentals.

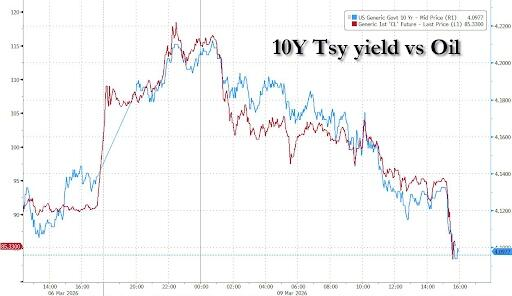

As fears of inflation subside, the 10-year US Treasury yield ended a five-day rising streak, falling 2.7 basis points intraday. The dollar index briefly surged nearly 0.8%, approaching last November 28 high, then retraced all gains, down 1% from the daily high.

( 10-year US Treasury yield vs crude oil price chart)

10-year US Treasury yield vs crude oil price chart)

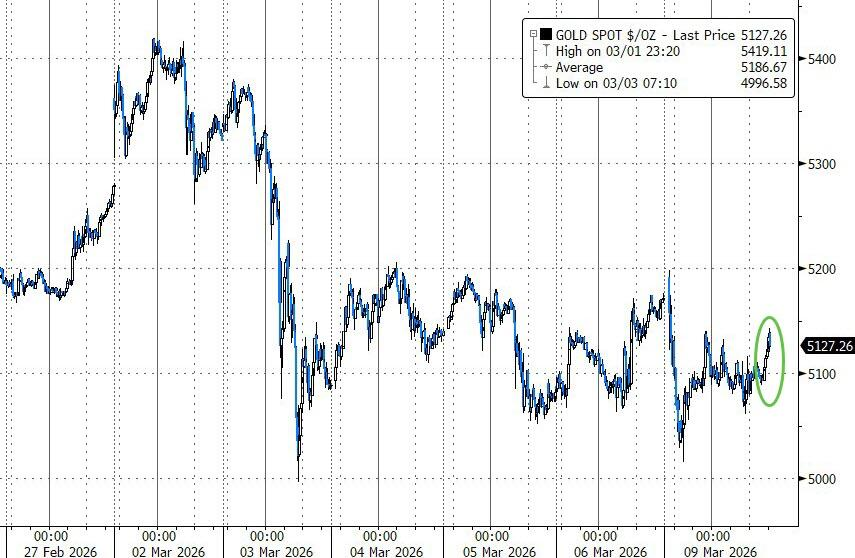

Spot gold also came under pressure during the early sell-off but rebounded as the dollar retreated from highs, ending the day down 0.7% from last Friday’s close. Spot silver reversed its intraday decline, rising over 3%. Among precious metals, spot palladium performed strongly, rising over 4% at one point.

( Gold price)

Gold price)

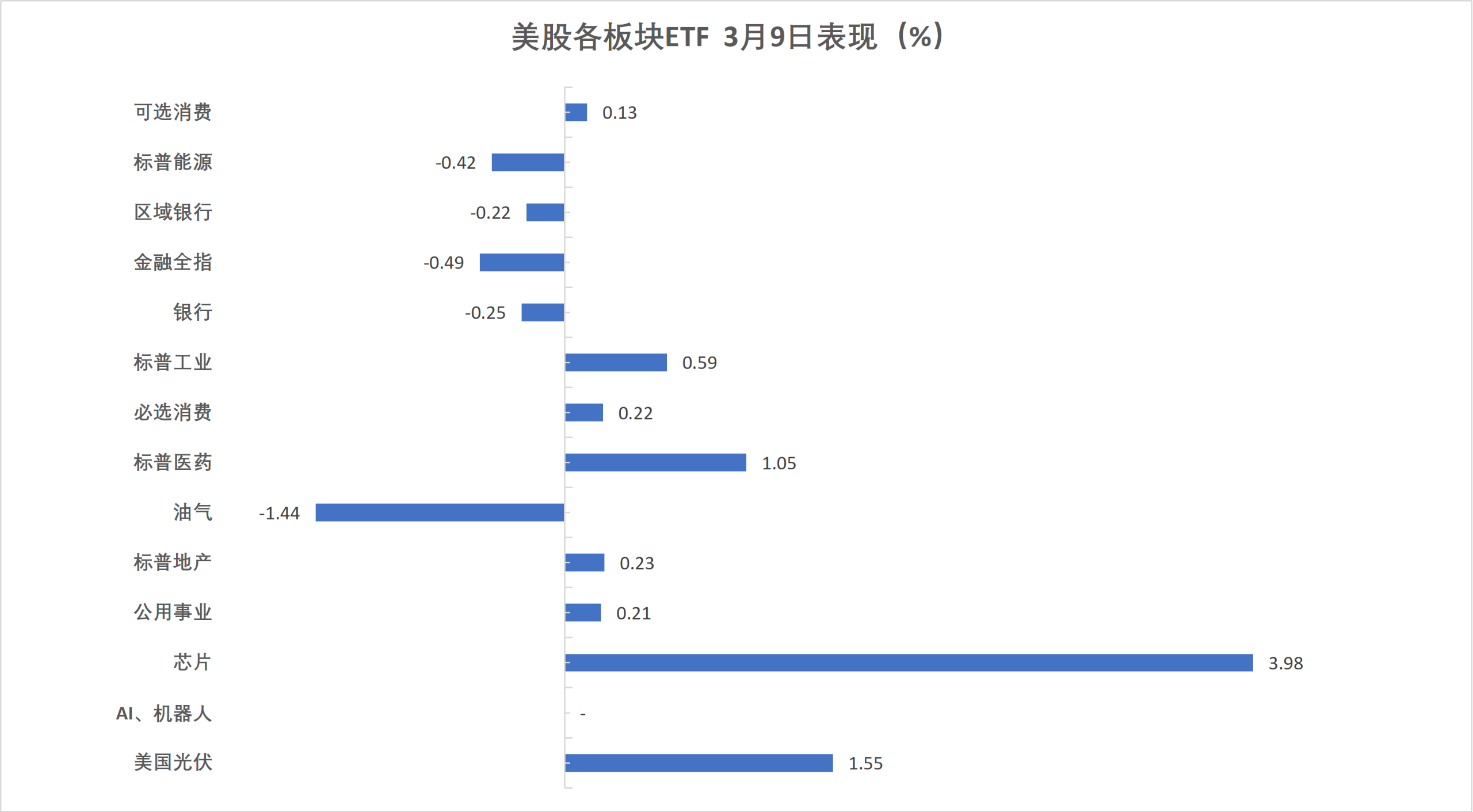

On Monday, all three major US stock indexes closed higher, with the S&P 500 up 0.8% and the Nasdaq up over 1.3%. Semiconductor ETFs gained over 3.6%, leading sector ETFs, while the S&P energy sector declined over 0.4%. Hims & Hers shares soared over 40%, and Novo Nordisk withdrew a patent infringement lawsuit previously filed against Hims & Hers.

( Sector ETFs as of March 9)

Sector ETFs as of March 9)

The “Magnificent 7” tech giants rose 1.34%, reaching 194.97 points, mostly declining during the day and surging after Trump’s speech at 03:19 Beijing time.

Chip stocks:

Philadelphia Semiconductor Index up 3.93%, at 7,810.40.

AMD up 5.33%, TSMC up 2.89%.

Chinese concept stocks:

Nasdaq Golden Dragon China Index up 1.76%, at 7,083.84.

Popular Chinese stocks: Xpeng up 6.4%, BYD up 6%, Meituan up 5.7%, Li Auto and NIO up over 3.8%, Baidu up 2.9%, Tencent up 2.4%, Alibaba up 1.4%.

Other stocks:

Eli Lilly up 1.82%, Berkshire Hathaway B shares down 0.36%.

Broadcom up 4.62%, Qualcomm up 1.78%, Adobe down 0.42%, Netflix down 0.71%, Oracle down 0.92%, Salesforce down 1.64%.

European markets closed at their lowest levels this year, down more than 6.1% from the all-time highs. France’s stock market fell nearly 1%, while Norway’s rose 0.3%.

( Major European indices performance on March 9)

Major European indices performance on March 9)

Sector and individual stocks:

Among Eurozone blue chips, Volkswagen fell 2.40%, Ferrari, L’Oréal, EssilorLuxottica, Adidas, and Ates Group declined between 2.08% and 2.19%.

All components of the STOXX 600 declined; Kinnevik dropped 16.97%, ArcelorMittal down 7.88%, Lufthansa down 6.38%.

US 10-year Treasury yield fell over 3.8 basis points, briefly dipping below 0.34% for the 2-year real yield. UK 2-year gilt yields narrowed their gains to 12 basis points.

( US key Treasury yields)

US key Treasury yields)

Eurozone bonds:

Germany 10-year yield down 0.1 bps at 2.859%, trading between 2.928% and 2.853%. The 2-year German bond yield up 0.6 bps at 2.318%.

UK 10-year yield up 2.0 bps at 4.647%. The 2-year gilt yield up 12.0 bps at 3.990%, remaining above 4.100% for most of the session before retracing gains from 21:00.

France, Italy, Spain, Greece 10-year yields opened high and declined, with a maximum drop of 1.1 bps.

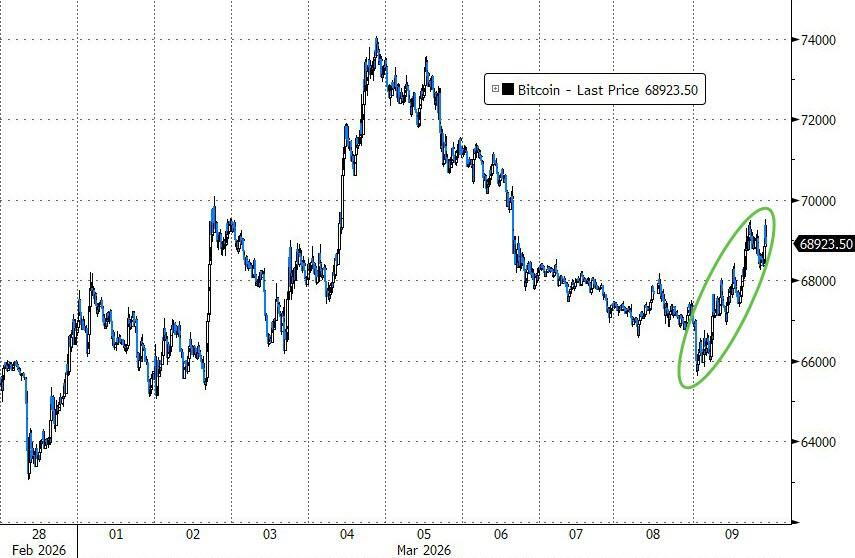

The dollar index briefly surged nearly 0.8%, approaching last November’s high, then retraced all intraday gains, down 1% from the high. Cryptocurrencies rebounded, recovering weekend losses, with Bitcoin up 2.63% intraday.

( Bloomberg dollar index)

Bloomberg dollar index)

Non-dollar currencies:

NY close: EUR/USD up 0.16%, GBP/USD up 0.29%.

Commodity currencies: AUD/USD up 0.73%, NZD/USD up 0.61%, USD/CAD flat.

JPY:

Offshore RMB:

Cryptocurrencies:

( Bitcoin price rally)

Bitcoin price rally)

Crude oil (WTI) surged nearly 30%, approaching $120. Following signals from G7 countries about possible strategic reserve releases and Trump’s hint that the war is ending, oil prices plummeted. US crude tumbled over 31% from the daily high and down 7% from last Friday’s close, while Brent crude fell 4.67%.

Natural Gas:

Spot gold was pressured during the early sell-off but rebounded as the dollar retreated from highs, ending down 0.7% from last Friday. Spot silver reversed its intraday decline, rising over 3%. Among precious metals, spot palladium performed strongly, rising over 4%.

Risk warning and disclaimer

Market involves risks; investment should be cautious. This article does not constitute personal investment advice and does not consider individual user’s specific investment goals, financial situation, or needs. Users should consider whether any opinions, views, or conclusions herein are suitable for their particular circumstances. Investment based on this information is at your own risk.