As the DeFi lending market has developed, the traditional lending model based on overcollateralization has gradually revealed its limitations in capital efficiency. For institutional borrowers, having to pledge large amounts of collateral not only increases financing costs, but also limits how flexibly they can use their capital. As a result, the market has begun looking for a more efficient on-chain credit model, one that allows institutions to obtain financing through credit, much like in traditional finance, rather than relying on heavy collateral requirements.

Maple Finance is an important innovator within this trend. By building Institutional Lending Pools, it connects capital from liquidity providers with the financing needs of institutional borrowers, while relying on professional Pool Delegates for credit review and risk management.

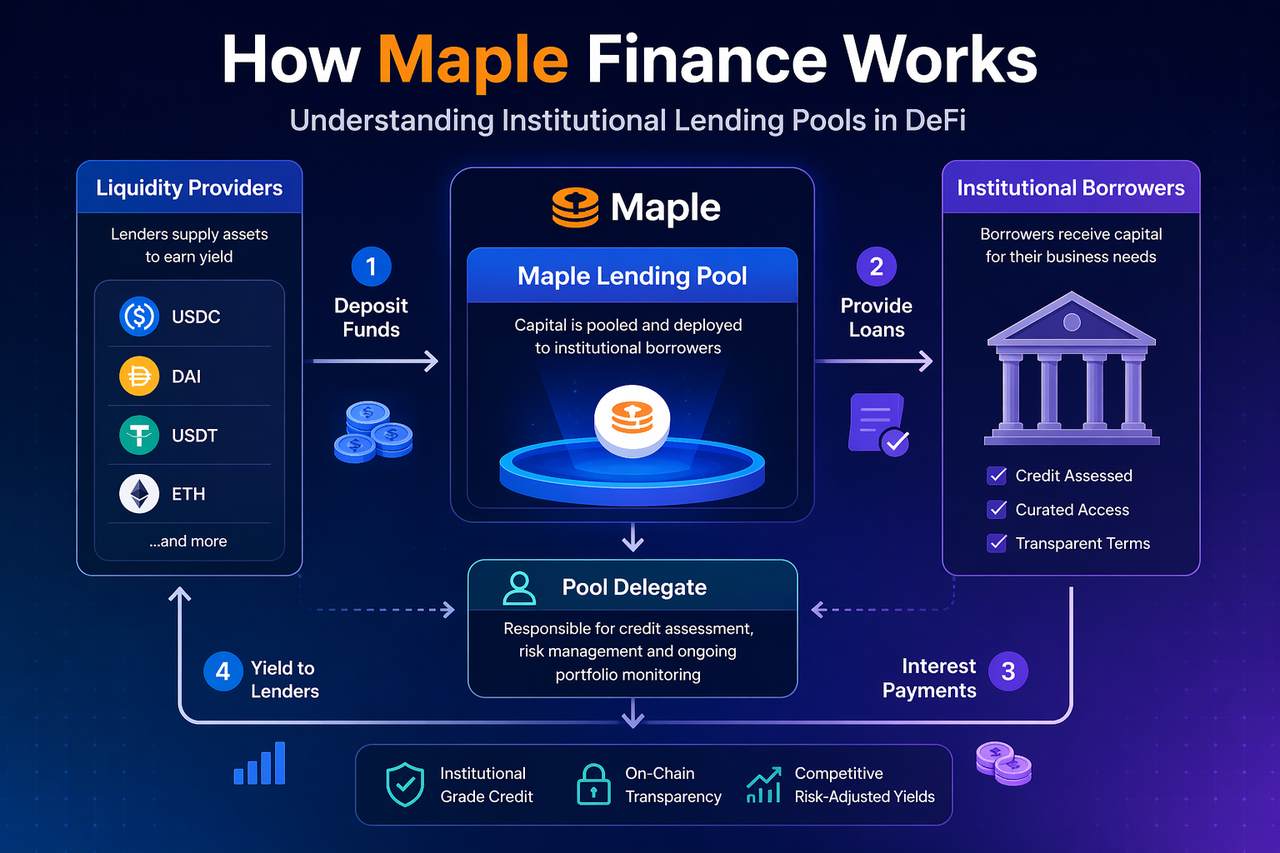

What Are Maple Finance’s Institutional Lending Pools?

Maple Finance’s core structure is the institutional lending pool, an on-chain capital pool where liquidity providers supply funds and institutional borrowers apply for loans. Once capital providers deposit assets into a lending pool, those funds are used to issue loans to approved institutional borrowers, generating returns for capital providers based on the loan interest rate.

Unlike traditional DeFi platforms, Maple’s lending pools are not fully open lending markets. Instead, they use a professional credit assessment mechanism to manage risk. Each lending pool has clear borrowing rules, a defined yield structure, and specific risk parameters, allowing liquidity providers to participate on-chain in yield opportunities similar to those found in institutional credit markets. This mechanism improves capital allocation efficiency and gives institutions more flexible access to on-chain financing.

What Role Does the Pool Delegate Play in Maple Finance?

The Pool Delegate is a key role within Maple Finance’s lending pools, responsible for borrower screening, credit review, loan term setting, and post-loan risk management. When an institution applies for a loan, it must submit financial and credit-related information to the Pool Delegate, who then assesses the borrower’s repayment capacity and default risk before deciding whether to approve the loan application.

This mechanism effectively brings the credit intermediary function of traditional finance into DeFi. The presence of Pool Delegates helps reduce default risk in lending pools and improves the quality of loan assets. For liquidity providers, this means they do not need to evaluate borrower risk on their own. Instead, they rely on professional managers for due diligence, allowing them to participate in on-chain yield opportunities with a higher degree of risk control.

How Does Maple Finance’s Lending Process Work?

Maple Finance’s lending process mainly consists of four steps. First, liquidity providers deposit funds into a lending pool, creating a pool of capital available for lending. Second, institutional borrowers submit loan applications, and the Pool Delegate reviews their qualifications and sets loan terms, such as the interest rate, maturity, and loan size.

Once the application is approved, the lending pool issues the loan to the institutional borrower. During the loan term, the borrower pays interest and repays the principal at maturity. The platform distributes interest income to liquidity providers according to preset rules, while the Pool Delegate collects a management fee. The entire process is executed automatically through smart contracts, improving the efficiency of capital allocation and ensuring that lending records remain transparent and traceable.

How Does Maple Finance Generate Returns for Liquidity Providers?

Liquidity providers earn returns on Maple Finance by supplying capital to lending pools. The interest paid by institutional borrowers forms the source of yield, and these returns are distributed to capital providers in proportion to their contributions. Because borrowers are typically institutional users, lending rates are often higher than those of traditional low-risk financial products, creating a relatively stable yield opportunity for liquidity providers.

In addition, Maple Finance’s yield model does not depend on token inflation incentives. Instead, it is built on real borrowing demand. This means the source of yield is more closely tied to genuine financial activity rather than short-term liquidity mining rewards. For on-chain capital seeking stable returns, this model has stronger sustainability and appeal.

What Are the Advantages of Maple Finance’s Lending Pool Mechanism?

The biggest advantage of Maple Finance’s lending pool mechanism is improved capital efficiency. Traditional DeFi lending depends on overcollateralization, while Maple uses credit review to give institutions a more flexible financing method, allowing borrowers to obtain loans at a lower capital cost. This model better fits institutional treasury management needs and brings on-chain lending closer to the logic of traditional finance.

At the same time, the lending pool structure gives liquidity providers a clear source of yield and a defined risk management framework. The professional review mechanism provided by Pool Delegates helps reduce default risk, while on-chain execution keeps the lending process transparent and efficient. By combining professional credit management with DeFi automation, Maple Finance serves as an important bridge for bringing institutional credit into on-chain finance.

What Risks Does Maple Finance’s Lending Pool Mechanism Have?

Although Maple Finance’s lending pool mechanism improves capital efficiency, it still carries credit default risk. If an institutional borrower cannot repay a loan on time, liquidity providers in the lending pool may suffer losses. While Pool Delegates conduct credit reviews, they cannot completely prevent borrower defaults.

Market liquidity risk and smart contract risk should also not be overlooked. When market volatility is high, liquidity exits may become limited, while smart contract vulnerabilities may affect fund security. Therefore, while pursuing returns, participants should also pay attention to lending pool quality, the reputation of the Pool Delegate, and the platform’s overall risk control capabilities.

Conclusion

Through its institutional lending pool mechanism, Maple Finance connects liquidity providers with institutional borrowers and uses Pool Delegates for credit review and risk management, creating an on-chain credit market with greater capital efficiency. Compared with traditional overcollateralized lending, Maple Finance is better suited to institutional financing needs and also creates more sustainable yield opportunities for capital providers.

As institutional capital continues to enter the DeFi market, Maple Finance’s lending pool model has the potential to become important infrastructure for institutional-grade on-chain lending.

FAQs

What Is the Pool Delegate Responsible for in Maple Finance?

The Pool Delegate is responsible for borrower review, loan term setting, and risk management, serving as the core credit manager within Maple Finance’s lending pools.

Where Do Maple Finance’s Returns Come From?

Returns mainly come from the loan interest paid by institutional borrowers. Liquidity providers receive income based on their share of the pool.

Traditional DeFi lending relies on overcollateralization, while Maple Finance uses a credit lending model, making it more suitable for institutional borrowers and improving capital efficiency.

Are Maple Finance’s Lending Pools Risky?

Yes. The main risks include borrower default risk, liquidity risk, and smart contract risk, although the Pool Delegate mechanism helps reduce some of these risks.